Good morning! We've reached the end of this four-day week.

I see that the S&P 500 is now only down by 5% year-to-date. A couple of weeks ago, it was down 15%. I'll chalk this up as a win for buy-and-hold!

President Trump has said that the current 145% tariff on China "will come down substantially - but won't be zero". I have my fingers crossed for a major U-turn by Trump, under pressure from many of his own supporters.

We are all done for the week, have a pleasant weekend!

Companies Reporting

Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

| WPP (LON:WPP) (£6.0bn) | Trading Update | Guidance reiterated. Q1 revenue less pass-through costs -2.7% LfL. Full-year guidance flat to -2%. | |

| Pantheon International (LON:PIN) (£1.26bn) | Monthly Performance Update | £20m of share buybacks so far, £50m allocated. NAV per share 501.2p, down 0.5% for the month. | GREEN (Graham holds) There's a small drop in NAV per share caused by currency movements. I've become a huge fan of this in recent months and am open to the idea of adding more. |

| Mobico (LON:MCG) (£362m) | Proposed Sale of North America School Bus | SP down 41% Upfront net proceeds £275-290m. Earn-out up to $70m. FY24 adj. op profit at lower end of guidance. | RED (Graham) [no section below] We haven't looked at this since November and unfortunately it has gone off the rails today. There is a mild profit warning on adjusted profits ("lower end of guidance"), a further warning that there will be "a significant statutory loss" for the numbers that aren't helped by adjustments, and a disappointing sale of the School Bus business vs. analyst estimates. £275-290m will be received for deleveraging but the outstanding debt pile was nearly £1bn as of the June 2024 interim results. Superficially this stock is cheap against EBITDA and adjusted earnings, but real profitability has been very difficult for the company to achieve ever since the Covid era. Given the dismal track record in recent years and the apparent continuation of this record, I'll slap this with a RED colour for the time being. |

| Evoke (LON:EVOK) (£216m) | Trading Update | Q1 adj. EBITDA significantly up y/y. Last 12 months adj. EBITDA >£330m, in line with guidance. | RED (Graham holds) The market is pricing in an equity raise and I don't disagree that this may be required. Evoke's debts start to mature in 2027 and then most of them fall due in 2028. |

Record (LON:REC) (£108m) | Expectations for full year revenues are unchanged. AUM up $0.4bn to $100.9bn. Net outflow $0.7bn. | GREEN (Graham) [no section below] As noted in January, I like this company even though its growth is very modest (if any). The slight increase in AUM in Q4 (to March), helped by exchange rates, masks some modest outflows. Performance fees remain small but continue to boost the overall result. With a strong, liquid balance sheet and an enviable track record of profitability, I'm a long-term fan here. References in today's statement to the company taking "no market or counterparty credit risk ourselves" are perhaps motivated by recent events at Argentex. The two companies have very little in common, despite both provide currency risk management | |

Oxford Metrics (LON:OMG) (£60m) | H1 in line. Revenue H2 weighted (“normal seasonal pattern”). Net cash £41m. | AMBER/GREEN (Graham to do) I think the glass is half-full with an impressive cash pile and continuing operations that have been profitable. It's all down to management to invest the cash wisely from here. | |

| Argentex (LON:AGFX) (suspended at £52m) | Update re: Possible Offer and Bridge Funding | IFX may offer 2.49p per AGFX share. Discussions at an advanced stage. "The most attractive immediate proposal for Argentex shareholders". £6.5m bridging loan at 15% included. AGFX CEO leaves the company with immediate effect. | NO COLOUR (Graham) [no section below] I don't see any point in putting a colour on this as the shares are suspended and there is little prospect of them trading again. Investors representing 58% of AGFX's shares have undertaken to support this potential offer and so it looks set to proceed if can get done before AGFX runs out of cash. AGFX shareholders have lost over 90% of value in a week, with effectively zero warning. This must go down as one of the most shocking collapses we've witnessed from a company that appeared credible. |

Naked Wines (LON:WINE) (£57m) | FY March 2025 in line. Rev c. £250m. Net cash £31m. FY26 guidance to be given in summer. |

Pantheon International (LON:PIN)

Up 1% to 278p (£1.27bn) - Monthly Performance Update - Graham - GREEN

(At the time of publication, Graham has a long position in PIN.)

I added this to my portfolio recently.

For reasons that aren’t very important (specific to my personal circumstances), but which I’d like to mention in order to help explain my decision to buy a trust, I was looking for an investment with the following characteristics:

Lower-risk than buying stock in a single business

Can still provide equity-like returns

For tax reasons, returns are to be generated through capital gains as much as possible, with as little income as possible.

I could have simply added more Berkshire Hathaway, but I already have enough of that. After a reasonable amount of searching, I decided to invest in PIP.

Pantheon International Plc (the ticker is PIN, but they refer to themselves as “PIP”) is a FTSE-250 investment trust, overseen by $55bn private equity firm Pantheon Ventures.

Income seekers can look away now: PIP has never paid a dividend and has no intention of ever paying one.

It has a net asset value of 501.2p per share or £2.3bn, according to today’s update.

However, it is currently trading at just 278p, with a market cap of £1.26bn. That’s a 44% discount!

Valuations are based on the numbers given by the underlying private equity managers to whom PIP has allocated funds. So it is reasonable for investors to be concerned that these valuations are uncertain.

The way I make sense of the valuation is 1) I check the average earnings multiple on which the valuation is based, 2) I check to what extent the portfolio is able to make sales at a premium to book.

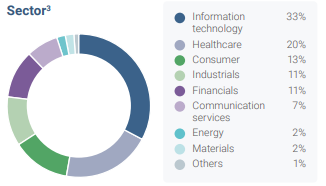

I think that on both accounts the stated net asset value appears pretty reasonable, although the impact of the recent trade fiasco on NAV is hard to quantify. 53% of PIP’s portfolio is in tech (33%) or healthcare (20%) with only 13% in consumer and 11% in industrials. My guess is that the first two of these sectors will do better in a high-tariff environment than the last two.

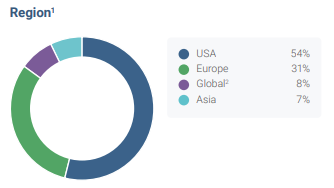

A slight majority of PIP’s investments are in the US:

I should do a deeper dive into PIP for you at some point in the future. For now, here are the highlights of today’s monthly update.

They start by acknowledging the discount:

The Board of PIP recognises that the discount on PIP's shares continues to be wide and this has been further exacerbated by market volatility.

They have allocated £50m to buybacks during the current financial year (FY May 2025), and £20m has been spent so far.

Today’s update shows a small (0.5%) drop in net assets per share for the month, primarily caused by foreign exchange movements which caused a 1.7% hit. Before currency movements, valuation gains were positive.

Balance sheet

PIP does use a small amount of leverage. Net assets as I’ve already stated are £2.3bn, but they have total private equity assets of £2.49bn. The ratio of net debt to NAV is 7.3%. Personally, I quite like this use of leverage. I think they can afford it, and it means that they never suffer any cash drag.

Diversification

Diversification is satisfactory: the three largest holdings in PIP’s portfolio are each worth a little more than one percent of the total portfolio. Everything else is worth less than 1%.

Diversification across PE managers is also pretty good: the manager with the largest percentage of PIP’s portfolio is Insight Partners, and they only manage 6.5%.

Graham’s view

I’ve become a really big fan of this in the last few months, and I’m open to the idea of adding more of it (it’s currently 4% of my portfolio).

I think it’s giving me access to a diversified range of high-quality private equity funds and private equity investments that have a good chance of providing strong returns, similar or maybe better than the major stock market indexes. PIP’s track record is 11.7% annualised NAV growth since 1987. The cherry on top is that the package is available at a very steep discount to NAV.

My own track record as a private investor is that PE-related shares have been my most successful investments. Volvere (LON:VLE) and Berkshire Hathaway (NYQ:BRK.B) have both been “baggers” for me, and are by far my largest holdings. Perhaps PIP can be the next one?

Evoke (LON:EVOK)

Down 1% to 47.4p (£220m) - Graham - RED

(At the time of publication, Graham has a long position in EVOK.)

This is a hair-raising situation where the company’s viability is seriously in question.

I gave it a RED in March, despite continuing to hold it as a stale bull. Its full year results were terrible, including huge losses and adjustments.

Even worse, the leverage multiple remained unacceptably high at 5.7x. Net debt was £2.1bn.

Today’s update strikes an optimistic tone. Here are some of the key points.

Revenue continues to grow at a modest pace, +2% at constant currencies. This is “in line with guidance” but the full year growth rate is expected to be “consistent with the mid-term target of 5-9%”. So improvement is expected and needed from here, in order to hit forecasts.

Adj. EBITDA last year was £312m, as the company beat guidance (which had already been upgraded) of £290-300m.

Today, the company says that Q1 revenue was “significantly higher year-on-year”, and that adj. EBITDA over the last 12 months is over £330m. This is also in line with guidance.

UK & Ireland online: I noted a very large fall in active players (-21%) as the company has dropped its previous marketing plans and focused on serving a smaller pool of more valuable customers. Average revenue per user is up 26%. Overall revenue down just 1%.

International: revenue +14% at constant currencies, boosted by an acquisition but seems to be doing well.

Retail (includes William Hill): revenue down 6%, some positive noises here:

The outlook for the remainder of the year is more positive with the roll-out of new machines completed together with the expected benefit of planned improvements across the sportsbook and overall in-store experience.

5,000 new gaming cabinets have been rolled out here.

CEO comment excerpt:

…While Q1 revenue was below our 5-9% annual growth target, Adjusted EBITDA is significantly higher year on year, with LTM Adjusted EBITDA reaching more than £330m. This reflects the Group's significantly more efficient operating model and our clear focus on creating value through sustainable, profitable growth.

…Whilst the UK&I Online and Retail performance was behind where we wanted to be in Q1, we have moved swiftly to improve some of the underlying drivers of the performance and have been seeing stronger trends in April…

Graham’s view

As I’ve said before, I probably should have sold this one already.

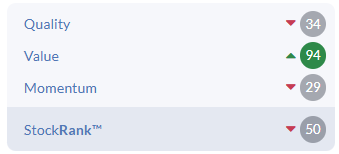

Overall, I agree with its StockRank categorisation as a Value Trap:

The notional P/E multiple of 3.3x is not real, given the plethora of adjustments that the company makes and of course the heavy debt load making this first and foremost a question of whether or not the existing equity can survive at all.

I still believe in the quality of the company’s assets: I like (and occasionally use!) the 888 online brand. William Hill is also a fine brand even if the quality of the retail business is no longer what it was. Mr Green also has a substantial audience.

So it’s a question now of whether adj. EBITDA can convert into enough real cash flow to start paying down the debt and achieve a reasonable leverage multiple.

According to the company’s current (downgraded) plans they are targeting leverage below 5x by the end of the current year, and then below 3.5x by 2027.

I have little faith that they can achieve this, but if they did then there is a good chance that the equity would be awarded a normal earnings multiple, and we’d see a substantial recovery.

The problem with being late in hitting their leverage targets is that it might cause trouble when it comes to refinancing. Their debt facilities start to mature in 2027 (€582m note) and then most of it matures in 2028. Their credit rating at Fitch is B+ (i.e. junk), with a negative outlook.

So the outcome here might very well depend on conditions in the debt markets in a few years - will banks and bondholders be happy to let them continue working away at this as they are, or will fresh equity be needed?

At the current market cap, investors are pricing in an equity raise and I can’t disagree that there’s a strong possibility this will be required.

Oxford Metrics (LON:OMG)

Unchanged at 48.4p (£60m) - H1 Trading Statement - Graham - AMBER/GREEN

Oxford Metrics plc (LSE: OMG), the smart sensing and software company servicing life sciences, entertainment, engineering and smart manufacturing markets, provides an update on trading for the six months ended 31 March 2025 ("H1").

We have a nice “in line” update today, although with an H2 revenue weighting that the company says is normal.

There is also pleasant news on the tariff front: they do not anticipate “a material impact” from tariffs at this stage.

Their motion capture technology is used in the life sciences sector, in entertainment, VR, etc, and they also have a new “smart manufacturing division”. Here is the update on business:

Momentum during the first half has continued across both divisions. Vicon secured new contracts across all main markets and in March, launched markerless motion capture. Vicon Markerless empowers creative and previsualisation teams to bring ideas to life with greater speed and ease than ever before. The build out of our smart manufacturing division has progressed with a number of new contract wins and the appointment of a new managing director, Dr Simon Gunter, to drive forward initiatives to capture more of this growth market.

Graham’s view

The major question - as highlighted by Roland in a brief section in February - is what the company might do with its cash pile. Today’s update informs us that this currently stands at £41m.

One thing they have been doing with it is buying back their stock on a regular basis - it looks like they have been authorised to buy back up to 10% of their shares.

Checking some of the history here, I see that the big cash injection happened in May 2022, when they sold their “infrastructure asset management division”. That deal took place under the previous CEO.

Three years later, I don't see much evidence that the current Board have been great capital allocators, but it might be too soon to tell.

The chart suggests that investors have not been overly impressed by developments:

While some of the cash is being returned to shareholders via the buyback, it looks like most of it will likely be spent on the smart manufacturing division, including on M&A to build out this division.

Overall, I’m inclined to leave our AMBER/GREEN stance unchanged as the cash does still cover two-thirds of the market cap here. Additionally, we’ve had profits from continuing operations for each of the last two years, according to the FY Sep 2024 results.

I think the glass is half-full, but I’m very unsure as to what the outcome for shareholders might be. It's all down to management to invest the cash wisely from here.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.