Good morning! We have a backlog section from Mark to kick us off today. And the Agenda is now complete.

1pm: all done for now, have a great weekend!

Edit to add: The Week Ahead has now been published with the economic calendar and next week's company announcements - see here.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

J D Wetherspoon (LON:JDW) (£681m) | Interim Results | H1 adj. PBT -8.6% to £33m. Wage costs to increase £60m. Outlook: “reasonable” outcome for FY25. | AMBER (Megan) However much I like Wetherspoons as a consumer and as a listed business, I am concerned that the challenges in the UK’s pub industry will continue to weigh on the performance for some time. |

| Asos (LON:ASC) (£304m) | Trading Update | SP +20% Expects significant improvement in profitability in H1. Stronger gross margin, lower markdown activity, cost discipline. H1 revenue inline, adj. EBITDA ahead of consensus (£34m). | AMBER/RED (Graham) [no section below] I'm going to leave this with a moderately negative view although I do very much approve of the company's strategy to focus on full-price sales and margins over empty revenues. However, at the top of my mind is the net debt position. This was last seen in region of £170m, excluding lease liabilities, after the sale of the Topman and Topshop brands last September. A moderately negative stance therefore seems to remain justified on the basis that this is A) a value trap according to the StockRanks, and B) is likely to still carry substantial debts. Hopefully it can turn into a true turnaround story but I'm not convinced that it's there yet. |

Ceres Power Holdings (LON:CWR) (£139m) | Final Results | Rev +132% (£52m). Adj. EBITDA loss £22m. Outlook: 2025 revenue broadly similar to 2024. | AMBER/RED (Graham) It's an exciting year for the company and I wish it well, but the financials as they stand do not yet inspire confidence. At least they appear to be moving in the right direction. |

National World (LON:NWOR) (£60m) | Final Results | Rev +9%, adj. PBT +16% (£11.1m). Guidance: to meet expectations. | PINK (takeover to be effective by 30th April if there is no further delay). |

Volvere (LON:VLE) (£40m) | Trading Update | NAV ps £17.19 (LY: £14.83). Net income £4.8m (LY: £2.7m). 2025: challenging due to labour costs. | AMBER/GREEN (Graham holds) |

Petrofac (LON:PFC) (£32m) | Financial Restructuring: Update | Defers publication of annual results. Shares to be temporarily suspended from 1st May. | RED (Graham) [no section below] Massive dilution incoming and hopefully the company will be on a more stable footing when that occurs. I stay RED until the procedure successfully completes. Existing shareholders to be left with 2.2% of the company. |

OPG Power Ventures (LON:OPG) (£18m) | Trading Update | SP +5%) | AMBER (Graham) [no section below] No firm view on this as I'm unfamiliar with it and it's involved in power generation in India. Company is bullish on macro with demand for power in India set to rise over the next 10 years. Claims to have net cash of £12.6m after paying down debt. Could be worth looking into but the usual health warnings re: foreign companies will apply. |

Backlog

Crest Nicholson Holdings (LON:CRST)

Up 8% to 164p - Trading Update - Mark - AMBER

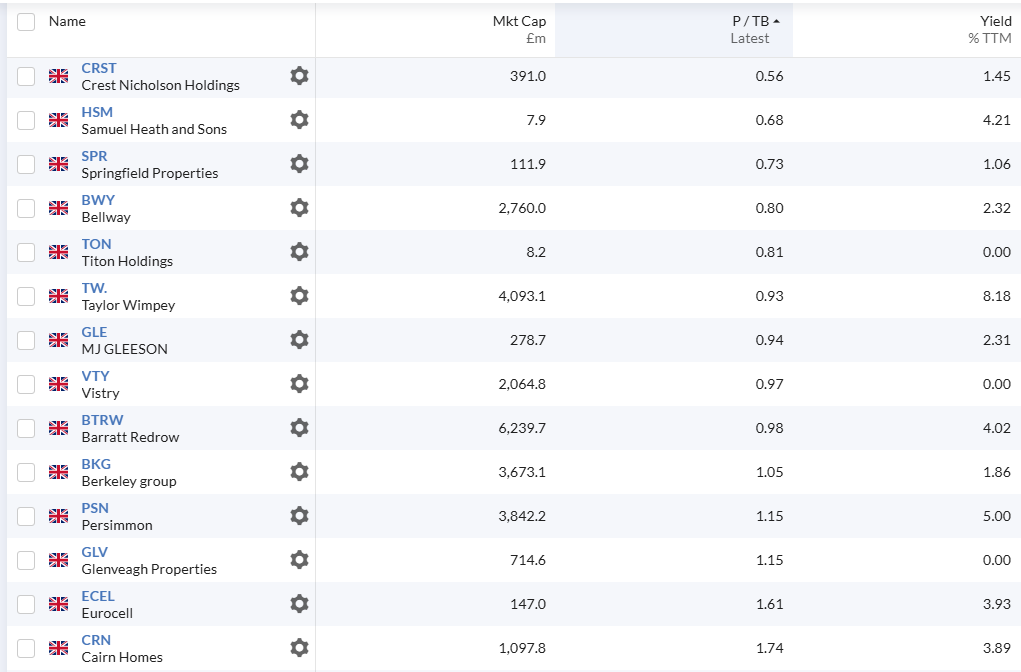

Crest Nicholson has been the cheapest housebuilder on TBV for quite some time:

However, many investors will say justifiably so, given those assets have been unproductive for some time now.

There is also the question of why they haven’t been acquired at this cheap level by someone who is operationally better. After all, there was interest last year that came to nothing. Do the industry experts know something about the company that we don’t? This may well be the large, and still not quite settled, amount the company has had to set aside for remediation of properties containing combustible materials (i.e. cladding.)

Putting that aside, today’s trading update shows that things might be about to turn for the company:

We have seen an encouraging start to the year. In the 10 week period to 14 March, the open market sales rate (excluding bulk) was 0.61 (FY24 0.50), supported by our self-help initiatives including ongoing training and upskilling of the sales team, revised incentive schemes and enhancing our product offering.

The Group has continued to drive higher levels of customer satisfaction achieving a score of 95.0% for the 2024 survey year (2023: 87.3%).

We remain on track to deliver results in line with guidance in the current financial year, with our cash performance tracking better than expected in the first four months.

It is not earth-shattering, but it is certainly good news for a company whose earnings consensus trend looks like this:

The market liked this update, with the shares rising about 8%. However, they would have to rise a further 40% to be on the P/TBV of the next cheapest housebuilder on this metric.

Mark’s view

The shares look too cheap on a P/TBV of around 0.5, assuming that is now a fair reflection of the fundamentals. If they can achieve the rating of cheapest housebuilder on this metric, then the shares rise around 40%. This trading update gives some hope that momentum may be reversing and that re-rating is on the cards, having looked doubtful for some time. However, the question of why the industry hasn’t closed the gap via corporate action remains. Graham rated this AMBER/RED following recent results due to the large and still variable provisions taken for cladding remediation. However, I think there is enough in today’s statement to consider a tentative upgrade to AMBER.

Graham's Section

Volvere (LON:VLE)

Up 7% to £19.30 (£43m) - Trading Update - Graham - AMBER/GREEN

(At the time of publication, Graham has a long position in VLE.)

This share is 30% of my single-stock portfolio, easily my largest holding, and so I should be considered biased. I’ve owned it since 2016.

Today’s update reads very positively, but most of us Volvere investors already had the impression that Shire Foods has been trading well.

The highlights:

Net assets per share, excluding the minority interest held by staff at Shire Foods: £17.19. This is an increase of 16% year-on-year. NAV had already increased by nearly 7% in H1.

Group net assets increased from £37.5m to £41.8m. The minority interest on the balance sheet is worth £3m+ so shareholder net assets are more like £38m.

Cash and available for sale investments increased from £23.7m to £27.8m.

Buyback analysis

Please note that the above progress was achieved in the context of the company spending £1.5m on share buybacks during the year.

Buybacks reduce net assets and they reduce cash.

However, they do increase net assets per share, when they occur at a discount to NAV.

In 2024, Volvere bought back its own shares at prices of £11.60, £14.50, £14.75, £14.80 (twice), £14.85 and £14.99.

It started the year with NAV per share (excluding minorities) of £14.83, and this had increased to £15.85 by the midpoint of the year. So it has been buying back below NAV.

Financial performance

Here’s the table:

Volvere only has one operating subsidiary, Leamington Spa-based Shire Foods.

They have been in the media twice this month. Firstly:

Warwickshire pie supplier celebrates growing Alid partnership (Warwickshire World)

Extract:

Shire Foods, based in Leamington Spa, is working with Britain’s fourth-largest supermarket to bring a brand-new range of Crestwood pies to Aldi shoppers this year.

The new pies, which include an exciting American-inspired flavour, will be available to buy in stores across the UK from May.

Shire Foods has partnered with Aldi since 2008 and is the supplier of its full range of Crestwood Frozen Pies, as well as popular baked items such as its Bacon and Cheese Wraps.

And secondly:

A humble pie with a unique filling and a taste loved by football fans across the West Midlands (Express & Star)

Extract:

The Balti pie is a creation which has become a staple of matchdays for so many football fans across the Black Country and across the country in general, with its warming taste helping many fans to battle the cold during games.

With the Black Country being an area with a high concentration of Indian restaurants, it would be tempting to suggest that the pie was created here.

However, its origins actually lie outside the Black Country in Warwickshire, where Shire Foods in Leamington Spa can lay claim to be the creators of the much-loved pie.

Shire has been on a very pleasing upward trajectory over the years:

2020 revenue £27.2m, adj. PBT £1.8m

2021 revenue £30.6m, adj. PBT £2.1m

2022 revenue £38m, adj. PBT £2.8m

2023 revenue £43m, adj. PBT £3.9m

2024 revenue £49m, adj. PBT to be confirmed.

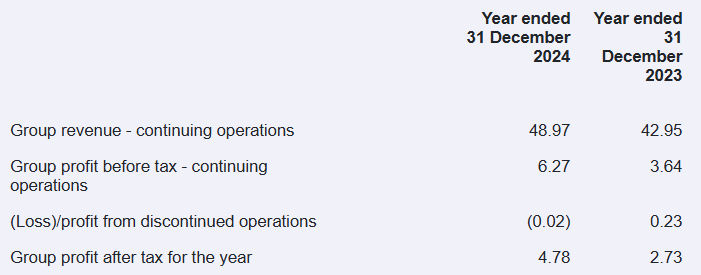

We don’t yet know Shire’s adj. PBT for 2024, but we do know that Group PBT has increased from £3.6m to £6.3m, and that after-tax profit has increased from £2.7m to £4.8m.

Group PBT, in addition to the Shire result, include items such as:

interest earned on cash

investment gains and losses

administrative expenses including the cost of Group management.

These items, excluding Shire Foods, are grouped together in a segment called “Investing and management services”. This segment was operating around breakeven in H1, whereas it previously operated at a loss when interest rates were lower.

So we’ll have to wait and see how exactly Group PBT of £6.3m was achieved. But nearly all of it should relate to Shire, as I expect that the result for the Investing and management services segment is likely to be around zero for the year.

Commentary

Nick Lander, brother of the late Jonathan Lander, says:

I am delighted with the performance for the year as a whole, which was underpinned by strong trading at Shire Foods and good returns on our treasury deposits. This is reflected in our increasing cash reserves, notwithstanding the significant treasury share purchases in the period.

He goes on to remind us that:

…there are industry-wide challenges in the form of increasing labour costs in 2025 because of the increase in the minimum wage, further compounded by the increase in employer's national insurance. The effect on Shire will be both internal and external, the latter from rising supply chain costs such as raw materials, packaging and transportation.

Despite the challenging environment, he does expect “a creditable performance” this year, and they continue to invest in additional capacity for future years.

On the acquisition front, he says that “we remain committed and poised” to invest if the right proposition is identified. But it has been a very long time since Volvere made a meaningful acquisition.

Graham’s view

The gains here have helped to bring my portfolio to life over the past year:

Looking forward, I have mixed feelings about continuing to hold this one.

On the one hand, we have the question of valuation. Cash and available for sale investments cover nearly two-thirds of Volvere's market cap. Unless or until this cash is invested, it backstops much of the value.

Net assets per share also support the valuation, with NAV per share (fully tangible) covering nearly 90% of the market cap.

The wildcard is what could be achieved if Shire Foods was sold.

In a sale, Shire Foods should not be sold for its NAV but instead (hopefully!) for a reasonable multiple of earnings.

Let’s take a £6m profit figure for example, which would be a trailing figure - hopefully 2025 might see some additional progress.

After tax that’s c. £4.5m.

An 80% ownership interest would leave £3.6m.

Is it crazy to think that someone might pay an earnings multiple of 10x to acquire this? Perhaps that’s far too optimistic, but what about 6x?

It’s not exactly the same sector but bakery group Finsbury Foods was acquired for £143m in 2023, on the back of PBT of £16m. That was equivalent to an after-tax earnings multiple of nearly 12x!

If Shire achieved a lowly multiple of only 6x trailing earnings, that would create a £22m valuation, which would see Volvere’s net worth shoot up to £50m. But I very much doubt that Volvere would be willing to sell at that price.

So on valuation, I don’t how see the Group as it currently exists after today’s numbers could be worth any less than £50m in terms of break-up value (that’s £22.70 per share). Given the trajectory of Shire, and the ability of other food manufacturers to achieve decent earnings multiples, I think a significantly higher number makes more sense in terms of fair value.

But (there is always a but!) my main doubt that I have around Volvere is that I can’t actually say that I support its continuation. If there was a vote tomorrow to change its strategy, to enable it to begin a wind-down process, I would support that.

For me, the point of this investment was to back the team (Nick and Jonathan). I’m very glad I did. They did a brilliant job. And I always approached this investment with a lot of patience, because I had faith in that team.

However, with Jonathan having very sadly passed away in 2023, my personal view is that Volvere is in need of a new strategy. My most preferred strategy would be for the company to very gracefully and very calmly call it a day. They don’t need to be in any rush to sell Shire Foods, in the same way that I have not been in a rush to sell my Volvere shares. But they could start the process of looking for an appropriate buyer. Perhaps the recent media articles are a way of discreetly attracting interest. We shall see.

Ceres Power Holdings (LON:CWR)

Down 7% to 66.3p (£128m) - Final Results - Graham - AMBER/RED

Horsham, UK: Ceres Power Holdings plc ("Ceres", the "Company") (CWR.L), a leading developer of clean energy technology, announces its audited results for the year ended 31 December 2024.

This collapsed nearly 40% in February when it announced the loss of its partnership with Bosch.

I took a moderately negative view, as the company’s enormous losses can at least be funded by its cash position (£102.5m as of Dec 2024).

Today we have full-year results, with the following highlights:

Record order intake £113m

Revenue more than doubles to £52m

Loss of £28m (2023: loss of £54m)

The cash outflow was £37.5m.

Outlook:

We end 2024 with a strong financial position and are well placed for significant growth in the future from existing licensees and future partnership prospects in both the SOFC and SOEC (solid oxide fuel cell and solid oxide electrolyser cell) markets. We continue to invest across the business to build a sustainable competitive advantage in highly differentiated solid oxide technology, which offers our partners the potential to industrialise and commercialise stacks and systems with superior efficiencies, reliability and economics for the low-carbon power generation and green hydrogen markets.

The CEO predicts that the first Ceres-based products will be available by the end of this year from Korean conglomerate Doosan.

Balance sheet has equity of £154m, with c. £134m of this being tangible.

Graham’s view

I wish this company well and I do think it’s an exciting moment for them with products hitting the market this year. It’s also undeniable that there has been some financial progress as the full-year loss has very meaningfully reduced. This is due to increased revenues from “technology transfers, development licences, engineering services and the provision of technology hardware”.

However, I do approach early-stage energy stocks with quite a lot of scepticism, as it seems that most of them don’t work out. Most early-stage companies don’t work out, but in many other sectors I find that the prospects of success are more amenable to analysis, at least for me.

For those of us who are unable to evaluate Ceres’ fuel cell/electrolyser technology, what we are left with are the company's financials. While these financials are on an improving trend, they are still deeply in the red. The cash balance, while impressive, will not last forever.

Therefore, I’m still AMBER/RED on this one. That’s consistent with the StockRanks - indeed, the StockRanks are even more cautious than I am.

Megan's Section

J D Wetherspoon (LON:JDW)

Down 9% to 541p (£727m) - Interim Results - Megan - AMBER

There aren't any massive surprises in this morning’s announcement from JD Wetherspoon, the owner and operator of just under 800 pubs in the UK. But the interim results have caused another big judder in the company’s share price.

The main concern is a further fall in pre-tax profits to £32.9m (from £36m in the first half of last year). The reason this is concerning is because this decline comes before the impact of higher national insurance contributions, which management has said will add £60m of additional costs per year.

In FY2024, the company only made £60m in pre-tax profits. The year to July 2025 will include four months worth of higher NI contributions (roughly £20m) which means current profit forecasts are probably a bit generous. More concerning is the outlook for the 2026 financial year, which will be the first to include a whole year’s worth of higher NI payments - which currently look meaningful enough to wipe out all of the company’s net profits.

Wage bills have already weighed on the company’s operating costs in the first half of the year, as has an increase in utility bills. Wetherspoons’ founder and chairman, Tim Martin, also points to the increasingly onerous tax burden facing companies in the sector as a reason for disappointing profits.

Mr Martin never shies away from an opportunity to take a pop at the VAT rates paid by pubs which, unlike supermarkets, have to pay VAT on food. And in these numbers he’s once again laid out the contribution his company (and his industry) makes to the public purse. VAT in the first half was £199m, alcohol duty £82m and corporation tax £11m (the latter is already more than the corporation tax in the entirety of FY2024).

Bigger property footprint means higher leverage

It’s a tax burden which Mr Martin says holds a big responsibility for the decline in the UK’s pub industry. A decline which Wetherspoons has attempted to take advantage of by expanding its own estate of pubs and buying up premises which it previously leased. Since 2010, the company has invested almost £500m in acquiring the freehold of pubs where it was previously the tenant. Just under three quarters of the pubs in the estate are now freehold, compared to 41% in 2010. The total value of the company's property, plant and equipment is £1.4bn.

But in doing so, Wetherspoons’ leverage has ratcheted up in recent years. Net debt (excluding lease liabilities) at the period end was £702m, slightly higher than the expected year-end net debt position and materially up from the £660m of net debt on the balance sheet at the end of FY2024. Net gearing, excluding the continuing lease agreements is 270%.

Cash flow troubles

These numbers also include an interesting comment on the company’s free cash flow conversion, which is expected to fall to about 100% of net profits. Management points to the fact that depreciation has and will continue to decrease because some of the older leaseholds have been fully depreciated. At the same time, reinvestment in existing pubs is likely to increase to an average of 3.7% of sales, from 3.1% historically.

These small tweaks are a bit of a moot point in these numbers, as the company reported a free cash outflow after investing £35m in the existing pub estate, £6m in IT services and reporting negative working capital.

Megan’s view

I am never that impressed when company management continues to point to external factors as the reason for underperformance, rather than addressing issues within their own control. But when it comes to Wetherspoons, I do have a spot of sympathy for Tim Martin.

The environment in the UK for owners and operators of pubs is not particularly friendly. Wetherspoons is not the only chain to be struggling and Mr Martin is using his position within the industry to argue the case for more support.

I also like Wetherspoons as a consumer. Mainly because you know what you’re getting - a cheap and cheerful pub, usually in a location that is exactly where you want a pub to be. But it is partly because of that strong identity that the costs of the NI rise are likely to hit the company quite hard. Passing on these additional costs to customers goes against what Wetherspoons stands for.

I do think that in the long-term there could be opportunities for the company to keep expanding as more and more peers go out of business. But there is too much of a storm to weather for now so I am going to stick on the sidelines. AMBER

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.