Good morning! It has been a hectic week for results, but we're expecting a quieter day today. Today's Agenda is now complete - and the report is now finished. Have a great weekend.

New Data Insights Article: please make sure you check out the Smart Money Playbook, which has just been published by Stockopedia:

In our latest deep dive, we’ve analysed a database of over 105,000 director deals, explored patterns in analyst recommendations, and assessed the investment habits of top-performing fund managers. The result? A data-driven guide to spotting and leveraging smart money movements—allowing you to make more strategic, confident investment choices.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Berkeley group (LON:BKG) (£3.3bn) | Trading Statement | Reaffirms earnings guidance - at least £975m of PBT across FY25 (£525m) and FY26 (£450m) | AMBER (Graham) [no section below] Profit guidance is impressive and puts the shares on a PER of about 10x for FY April 2026. Berkeley have been aggressively buying back their shares but the share price has been above the stock's last-reported NAV so this isn't helping to grow official NAV. At this earnings multiple and with no discount to official NAV, I can't get away from a neutral stance. |

Bodycote (LON:BOY) (£1.14bn) | Full year results | SP down 7% | BLACK (AMBER) (Graham) [no section below] This is now a little lower vs. when we looked at in November. A recovery in market conditions is taking longer than anticipated and profitability is standing still while the company goes about a restructuring programme that includes plant closures and operational performance improvements. There is now a small net debt position (£68m) vs. net cash last year. It spent nearly £60m on buybacks in 2024 and continues to buy them back today, and I'm not sure that its shares are sufficiently cheap to justify this. I downgrade my stance to neutral to reflect today's disappointing guidance. |

Target Healthcare Reit (LON:THRL) (£564m) | Half-year Report | Net tangible assets +1.8% to 112.7p (SP: 90.8p). “Growing rent roll and stable valuations”. | GREEN (Graham) I like this category of real estate and the discount to NAV on offer here, even after the share price recently rose from 83p to 91p. |

Science (LON:SAG) (£190m) | Increased shareholding in Ricardo (LON:RCDO) | Now owns 15.2%. Criticises RCDO board. | AMBER/GREEN (Graham) I'm downgrading our stance on Science as they have now spent a very large portion (over £20m) of their net funds on this exercise, and it's not clear to me how they intend to increase the value of Ricardo (apart from agitating for the removal of some directors, presumably). |

Vanquis Banking (LON:VANQ) (£141m) | Results for year ended Dec 2024 | On track for low single-digit ROTE in 2025. Due to headwinds, mid-teens ROTE in 2027. | BLACK (AMBER) (Graham) I want to be positive on this but we have a profit warning today with a more gradual recovery in the company's performance now forecast. I have to respect the trend and that means I can't turn positive on it yet. |

Life Science Reit (LON:LABS) (£136m) | Commencement of Strategic Review | SP has traded at significant discount to NAV for a prolonged period. Formal sale process. | AMBER/GREEN (Graham) This doesn't strike me as a particularly attractive REIT. It's too small and not diversified enough. But it is now up for sale and perhaps they can arrange a sale at a smaller discount to NAV than the current share price. |

Iqe (LON:IQE) (£125m) | Closing of Convertible Loan Note Financing | Raised aggregate proceeds of £18m. | RED (Graham) An implied interest rate of 18% is being paid. The Exec Chair invests £200k. I much prefer the position of the lenders to the equity. |

Backlog

Glenveagh Properties (LON:GLV)

€1.51 (€842m / £687m) - Final Results - Graham - AMBER/GREEN

I was AMBER/GREEN on this Irish homebuilder last year with it trading at a PER of below 8x, although it was trading at a premium to book value.

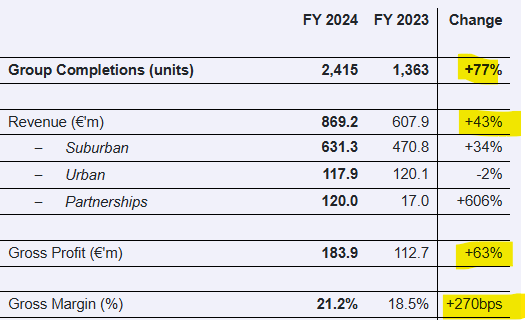

Yesterday’s full-year results showed net assets of €751m (Dec 2024), up from €682m (June 2024).

After-tax profits for the year were an impressive €98m. Full-year EPS guidance was achieved of 17 cents per share.

Year-on-year progress is fabulous: far more completions leading to huge revenue growth and at a higher gross margin:

Return on equity jumps from 7% to 14%.

Net debt of €179m is up year-on-year but it did fall in H2 (from €244m at the half-year).

Outlook:

The outlook for Glenveagh remains exceptionally strong, underpinned by a resilient demand environment, clear policy visibility for the next five years, and our ability to deliver the right product-principally high-quality, own-door housing-in the best locations.

EPS guidance for the current year is 19.5 cents. The order book is up 35% since March 2024, to €1.1 billion.

CEO comment:

"2024 was a landmark year for Glenveagh, defined by the successful execution of our Building Better Strategy and our agility in securing long-term growth opportunities. We scaled the delivery of high-quality sustainable homes, embedded innovations and efficiencies across our operations, and established Glenveagh as a preferred public sector partner.

Graham’s view

This continues to trade at a premium to book but the earnings multiple is still below 8x, taking into account the latest share price and the guidance for the current year.

I’m therefore inclined to leave my moderately positive stance unchanged.

Glenveagh enjoys excellent momentum in very favourable conditions - with demand for new homes (and homes in general) increasing much faster than supply, and a settled political situation after a recent election.

Graham's Section

Iqe (LON:IQE)

Up 5% to 13.55p (£131m) - Closing of CLN Financing - Graham - RED

We mentioned this in February when the plans were first announced.

The new 12-month notes are convertible at 15p.

They don’t pay interest but they have a face value of £21.2m, while they are being sold for only £18m.

This means that if they are repaid in cash in 12 months, the return for holders will be nearly 18%.

If the company extends the maturity for another six months, they will have to pay an additional premium of 9% to holders.

The Exec Chair (who currently owns no equity in IQE) has invested £200k in these notes. A NED with a modest holding has invested £80k.

Update on Strategic Review

As part of the Strategic Review, IQE has broadened its options in relation to the proposed IPO of IQE Taiwan to include the possibility of a full sale of IQE Taiwan. The Board believes there is a significant market opportunity in IQE's core operations and remains focused on reducing its cost structure for profitable growth, servicing its customers and maximising value for shareholders.

Exec Chair comment

"We are pleased to have closed our convertible loan note fundraising, which will significantly strengthen our near-term financial position. This reflects the support we have from our shareholders, who recognise the significant market opportunity for IQE and its long-term strategy. Our Strategic Review will enable IQE to unlock the significant unrealised value within the business and ensure it is able to invest in its growth strategy."

Graham’s view

As I said last time, an interest rate of 18% implies desperation. When that rate is being paid along with a conversion option, it’s even worse (because a conversion option should allow the borrower to access a lower rate than they would otherwise be able to!).

If I was asked my view on the convertible note or the senior debt (provided by HSBC), I’d probably be neutral. These debts are secured on IQE’s assets, and these lenders can look forward to getting paid from the proceeds of the sale of IQE Taiwan (although the value of this asset isn’t clear to me). HSBC in particular, as the senior lender, enjoys a great deal of security.

The last-published balance sheet for June 2024 showed tangible net assets of about £120m, mostly in the form of PPE at this capital-intensive business.

So the lenders are probably doing fine.

But I can’t say the same for IQE’s equity. For many years the business has struggled to generate a good return on its assets, and its poor financial performance has now resulted in a constrained cash position.

In the most recent interim results, the directors acknowledged that in a “severe but plausible” downside scenario, its liquidity and covenant headroom would be “tight”.

I see little choice but to remain RED on this for now. Perhaps a windfall from the sale of IQE Taiwan might help to turn things around?

Life Science Reit (LON:LABS)

Up 8% to 42p (£146m) - Commencement of Strategic Review - Graham - AMBER/GREEN

Here we have another REIT that might be leaving us. In this case, they are voluntarily hoisting up the “For Sale” sign due to frustration with their share price:

Since the Company's IPO in November 2021, it has fully invested its IPO proceeds in a high-quality portfolio of assets located in the "Golden Triangle" research and development hubs of Oxford, Cambridge and London's Knowledge Quarter. All properties are either leased, or intended to be leased, to occupiers in the life science sector and 55% of rent is derived from life sciences occupiers.

It’s another 2021 IPO that hasn’t worked out:

Problems they’ve faced include “higher inflation and elevated interest rates which have driven a fundamental slowdown in leasing activity and negatively impacted investor sentiment”.

These factors, coupled with the Company's size and low levels of liquidity have led to an underperformance of the share price, which has, as a result, traded at a significant discount to net asset value for a prolonged period of time.

At the interim results, NAV per share was calculated at 76.4p. Using real estate accounting (EPRA rules), net tangible assets were slightly lower at 75.5p. The latest share price is only 42p.

Leverage does not seem overly high: loan-to-value was 28%.

They reveal that they’ve been talking with potential acquirors:

Further to a number of discussions with potential acquirors in recent months the Board has confidence that, in the context of a strategic review, the business should be attractive to multiple parties if the outcome of the strategic review leads to the sale of the business.

Trading update: dividends are suspended until the strategic review has been concluded. There have been delays in leasing activity, and they expect that lease incentives will be required to secure further leases.

The latest figure for net tangible assets is 74.4p.

Graham’s view

I’m happy to take a moderately positive stance on this due to the modest leverage it uses and the significant share price discount offered against net tangible assets.

My impression is that LABS’s tenants are probably less reliable and more difficult to secure than we saw at the likes of Care REIT (LON:CRT), which has been covered here recently.

42% of the rent comes from the biomedical sector, 42% from technology, and 10% from quantum computing.

Occupancy was last reported at only 82.5%.

For a REIT it is sub-scale with only five finished assets and with its largest occupiers generating very large percentages of its total rent (#1 provides nearly 27%, and #2 provides 10%). This doesn’t provide the type of diversification across different assets and different tenants that a REIT typically should.

Therefore, while I do not view this as a particularly attractive REIT, it is now up for sale and very lowly valued against its balance sheet. So I think I can be moderately optimistic on prospects from here.

Vanquis Banking (LON:VANQ)

Down 10% to 49.4p (£131m) - Results for the year ended 31 Dec 2024 - Graham - AMBER

These results for 2024 are very poor, but I think are in roughly line with expectations. See our coverage last November, when the expected pre-tax loss for 2024 was £34.7m. The actual pre-tax loss is £34.8m.

The statutory loss for the year is worryingly large at £136m, higher than the current market cap! It include over £70m of impairments as Moneybarn has been written down..

Balance sheet tangible net asset value has reduced but is still significant at £359m. As I expressed last time, Vanquis shares are trading as little more than options on the company’s balance sheet.

We also have a profit warning today when it comes to future guidance.

Some snippets from the guidance:

Given the 4% decline in gross customer interest earning balances in 2024, FY26 balances are expected to be at the lower end of the previously guided range of £3.0bn to £3.5bn, reaching c.£2.6bn by the end of 2025.

And:

The Group continues to guide to a low single-digit ROTE in 2025. The trajectory of interest earning receivables growth means the Group now expect to achieve sustainable mid-teens ROTE in 2027, with low double-digits ROTE delivered in 2026.

With more growth expected to come from lower-risk but also lower-margin Second Charge Mortgages, Vanquis reduces its guidance for net interest margin.

Estimates

Shore Capital has made some large cuts to profit guidance: 2025 adj. PBT gets cuts by 40% to £10.5m, and 2026 adj. PBT gets cut by 20% to £59.7m.

Graham’s view

I’m generally positive on cheap lenders in the current environment, and Vanquis is one of the cheapest.

Also, after taking big impairments and write-offs, it promises that future results will be much cleaner, with adjusted performance “much more closely aligned with statutory performance”.

Another positive is that Vanquis did not pay discretionary commissions for motor finance loans, so it does not have to worry about the FCA investigation into that area. And it says that it made disclosures to customers re: commissions, which might protect it from the Court of Appeal ruling.

However, this is still a turnaround story and it strikes me as being a more complicated situation than most of the other lenders we’ve reviewed in this report.

I would like to upgrade my stance on this, given the very steep discount to book value and the potential for it to meet 2026 forecasts which would put it on a PER of less than 3x.

However, the business remains deep in turnaround mode and I still don’t trust the earnings forecasts. Note their negative momentum:

When it comes to value, I do have a positive bias on Vanquis but I’d like to have some conviction that the earnings forecasts have stabilised, before turning positive.

For now, with a fresh profit warning, I have to respect the trend and so I can’t turn positive on it yet.

Science (LON:SAG)

Unch. at 424p (£190m) - Increased Shareholding in Ricardo plc - Graham - AMBER/GREEN

Science continue with their hostile purchasing of Ricardo shares. They now have a 15.2% stake.

They take the opportunity to slam the Ricardo board of directors:

It is unfortunate that [Ricardo] has been negatively impacted in recent years by the board's strategy, weak operational performance with inadequate focus on profitability and cash flow, excessive executive remuneration and ineffective governance.

The substantial value destruction has resulted in an exodus of institutional shareholders despite share price levels being around their lowest levels in 15 years, a clear vote of no-confidence in the Ricardo board. It is similarly notable that no Ricardo board directors have accepted responsibility for the failure of governance by offering to resign. Ricardo shareholders should hold the board to account.

We’ve been GREEN on Science and AMBER/RED on Ricardo.

However, I’m really tempted to downgrade my stance on Science today.

I’m not a fan of hostile approaches. Unless there is a swift resolution, they generate more heat than light: lots of acrimony, lots of controversy, and lots of energy spent that might have been more productively used elsewhere.

Science has now spent nearly £22m on Ricardo shares.

It reported net funds of £26.8m as of Dec 2024, and is also spending these funds on a share buyback programme of up to £10m. So I’m not sure if it’s going to have net funds for much longer.

And it’s not clear to me how Science believe they are going to be able to “fix” Ricardo. Have they been speaking with other Ricardo shareholders?

I am going to downgrade our stance on Science today, as I fear that this adventure might ultimately turn out to be a misadventure, a distraction from their own business, and a poor use of funds. Hopefully I’m wrong about that. But the outcome of their current course of action strikes me as highly uncertain.

So far, the market is not impressed by what they’re doing:

Target Healthcare Reit (LON:THRL)

Unch. at 90.8p (£563m) - Half-year Report - Graham - GREEN

This REIT focuses on care home real estate. Today we have in interim report:

Influential sectoral tailwinds and a business model focussed on high quality, purpose-built real estate combine to deliver further earnings and NTA growth

Some key points:

Net tangible assets are up 1.8% to 112.7p

Total return including dividends of 4.5%

The loan-to-value is low at 22.7% and the average cost of debt is also low at 3.95%.

Over 90% of debt is hedged against rate movements until expiry, and the average term to maturity of their debt is 4.7 years. So they should enjoy these low rates for at least several more years.

Their portfolio diversification is not bad: 34 tenants across 94 properties. And the average unexpired lease term is excellent at 26 years.

Comment by the Chair:

"Target Healthcare REIT plc has continued to deliver both consistent property and financial performance, which is a testament to the quality of our business model, portfolio, and management team. We have a secure, long-duration income stream which provides compounding growth annually, which is underpinned by a portfolio containing some of the highest quality real estate in the care home sector. The modernity of the portfolio is evidenced by having one of the strongest EPC ratings of any UK listed real estate company."

Share price discount to NAV is 19.4% based on the latest share price and the NET per share announced today.

The Chair acknowledges that the discount is “persistent” and addresses it as follows:

Along with income-producing real estate companies more generally, our share price has been closely correlated with movements in interest rates and our discount to NTA therefore remains persistent as interest rates remain elevated. The sentiment towards real estate generally remains bearish given the economic outlook, though with positive sectoral demographics, consistently strong property performance and RPI-linked contractual rental growth, we remain well positioned for the future.

Graham’s view

I’m happy to give this a GREEN as the care home sector, like other healthcare categories we’ve recently covered here, strikes me as an attractive part of the real estate market. I agree that demand will inevitably increase. This REIT also has the attractive feature of super-long leases.

The only thing to watch out for is that care homes can sometimes be financially unstable, and so the tenants might be expected to change from time to time as ownership changes hands. But I think someone will still pay the rent to the property owner.

As with most REITs, interest rates may be the factor that ultimately closes the discount, rather than anything the company itself does or doesn’t do.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.