Good morning! We've reached the end of another tumultuous week in the markets.

The FTSE rose 3% yesterday and is set to open up by another 1% this morning, around the 8000 level.

After the dramatic announcement yesterday of a "90 day pause" on Trump's tariffs, excluding China, today is shaping up to be a quieter day for headlines.

2pm: I've made a clean sweep of today's announcements. Have a relaxing weekend - I think we all deserve it!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

BP (LON:BP.) (£54.9bn) | Upstream production lower quarter-on-quarter. Gas/low carbon energy: realisations broadly flat. Net debt up $4bn due to working capital build. | AMBER (Graham) [no section below] Sentiment around BP has been poor, especially in comparison with Shell (LON:SHEL), rightly it seems as BP's earnings forecasts have been slipping for some time. Today's guidance for lower production, partly due to divestments, looks to have been priced in already. BP had net debt of $23 billion at the end of 2024 and the $4bn increase in Q1 is expected to reverse. It has an investment-grade, single-A credit rating from all ratings agencies and so it should be reasonably secure. Since it's a resource stock, I take a neutral stance by default. | |

Niox (LON:NIOX) (£280m) | SP down 20% | AMBER/GREEN (Graham) Some pros and cons here. The potential PE buyers have walked away, and the stock is undoubtedly expensive against short-term earnings. At the same time, the company's growth and improving quality up to this point are intriguing. | |

Helical (LON:HLCL) (£215m) | SP up 5% Forward sale of a joint venture (City office, 100 New Bridge Street) for £333m. Will distribute 50-100% of net profits to shareholders. Net debt currently £127m. | AMBER/GREEN (Graham) [no section below] Taking a moderately positive stance here as the entire REIT sector appears undervalued. Helical's most recent interim results showed net tangible assets of £408m (331p) and thanks to disposals, their pro-forma loan-to-value was only 15.9%, "its lowest ever level". The sale announced today is expected to trigger shareholder returns after it completes in April 2026. This stock carries additional risk due to its small size and dependence on the success of a small number of large projects, but I expect that the £215m market cap leaves scope for plenty of upside if they progress as planned. | |

Optima Health (LON:OPT) (£150m) | Acquires Cognate Health for up to €9m, adding €7m revenue and €1m EBITDA. Cognate earned PBT of €0.86m in 2024. The Board will continue to evaluate bolt-on acquisitions. | AMBER (Graham) [no section below] This provider of employee health and wellbeing services only listed in October 2024, when it demerged from Marlowe (LON:MRL). The acquisition today relates to a company providing very similar services in the Republic of Ireland, expanding Optima's geographic reach and customer base, and enabling it to more easily serve customers with employees in both jurisdictions. I think the valuation at 9x EBITDA (assuming a full earn out) is probably fair and the rationale makes sense. I'm neutral on Optima until it develops more of a track record as a standalone entity and I have more time to evaluate it. | |

Kistos Holdings (LON:KIST) (£101m) | 8,050 boepd, in line. Adj. EBITDA $95m. Statutory loss $52m. FY25 production guidance reiterated. | AMBER (Graham) no section below] No particular view on this company, but I note that it's the current vehicle of Andrew Austin (17% shareholder). While running iGas Energy, he transferred £10m of iGas shares to an American firm, Equities First Holdings LLC. The arrangement was described as loan to fund the acquisition of iGas shares, but that's not how I interpret it. Equities First was the same firm used by Quindell's Rob Terry. I personally wouldn't touch the stock of any company managed by CEOs who have used Equities First. Although those who got involved with Austin's subsequent company, RockRose Energy (RRE), did very well indeed. Let's hope he can guide Kistos to similar success. | |

Character (LON:CCT) (£47m) | Withdraws market guidance for FY25. USA 20% of sales. Still confident company will be profitable for this financial year. | AMBER/GREEN (Graham) Downgrading this Super Stock by only one notch as the tariff problem is contained to a modest portion of their total sales and their cash position should help them get through this. | |

Ondo InsurTech (LON:ONDO) (£47m) | Revenue +40% (£3.8m). EBITDA positive by end FY March 2025. Cash £4m (before the repayment of a £1.3m loan note). | AMBER/RED (Graham) [no section below] I'm going to downgrade this a notch to AMBER/RED as the assumptions behind a valuation at such a high multiple of sales must be terrifically bullish. The company says that "annualised contracted recurring revenue" is now £5.9m but this includes the revenues for a pilot scheme. If the pilot is successful then all bets are off but for now the cash balance isn't particularly high (less than £3m) for a company that is expected to remain loss-making for the next couple of years, even if it is producing positive EBITDA on a run rate basis by the end of the current year. | |

XLMedia (LON:XLM) (£13.4m) | They will buy back up to 70.9% of their shares at 11p. No further distributions prior to suspension. | PINK (Graham) Company suggests that the returnable cash value is no more than 10p in their base case scenario. So the 9.8p share price is fair enough. |

Character (LON:CCT)

Down 7% to 240p (£44m) - Trading Update - Graham - AMBER/GREEN

I’m getting vibes similar to 2020 when I read some of the announcements this week. The macro situation has made it impossible for some companies to make forecasts regarding their future performance.

That’s the case with Character, designer and distributor of toys and games. Their manufacturing takes place in China and as they outline today, 20% of sales are to the US and now presumably subject to a 145% import tariff.

The Board's visibility for forecasting sales to USA (which were c.20% of Group turnover in the last financial year) and its ability to assess the financial implications for the Group have been considerably obscured by these events. Consequently, the effect of the imposition of the trade tariffs will be felt in the second half by the Group and, as a result, the Company is withdrawing the market guidance for the year ending 31 August 2025. Despite this, the Board remains confident that the Group will be profitable for the current financial year as a whole.

For H1 (the six months to February), trading is anticipated to be in line with H1 of the prior year, when adjusted PBT was £2.1m.

The Board is confident that Character can “ride out the storm”.

Prior Forecasts

Checking the forecasts that were in place prior to this update, I see that FY25 was expected to be very similar to FY24. For example from Allenby:

FY25 revenue £123m (FY24: £123.4m)

FY25 adj. PBT £6.7m (FY24: £6.6m)

Net cash was forecast to increase from £13m to £16m. As I noted in January, the company has been spending some of its funds on a £2m buyback.

Graham’s view

I am often inclined to treat the withdrawal of guidance as worse than a profit warning - as I would much prefer to have a guide for how bad things are, rather than no guidance at all!

In the case of Character today, however, the blow is softened by a number of factors:

Affected sales are a somewhat small (20%) portion of their total sales.

We have guidance that they will still be profitable for the year as a whole (although this does give leeway for a loss in H2).

Their healthy cash balance should help them through this difficult period.

Therefore I’m happy to downgrade this by only one notch to AMBER/GREEN.

This reflects the risk that lost sales to the US could be very costly in the short-term. For example, the risk of an inventory build-up or agreements with manufacturers that need to be restructured. It wouldn’t surprise me if Character lost about a year’s worth of profits and was still dealing with the fallout of this problem a year from now.

For now, the share price is refusing to fall out of the bottom of the range it’s been in for last two years:

Especially considering the company’s cash balance, I’m comfortable retaining a moderately positive stance here. But maybe they should consider a 90 day pause on buybacks?

XLMedia (LON:XLM)

Up 3% to 9.8p (£14m) - Tender Offer - Graham - PINK

I noted last week that XLM had funds higher than its market cap, and was sending cash back to shareholders. But this isn’t a type of trade that I go for these days, having learned the hard way that taxes, costs and delays often lead to disappointment.

This paragraph in today’s announcement is key, discussing potential tax liabilities:

While there is potential for both upside and down side to these calculations, in its base case scenario, the Board does not expect there to be more than approximately 10p per Ordinary Share of returnable cash value remaining in the Company assuming full take up of the Tender Offer. Further returns, if any, will follow settlement of the Company's liabilities as part of the liquidation process.

The tender offer announced today is at 11p per share, but it’s only for 70% of the company’s remaining shares.

The remaining 30% of shares will be suspended and then I guess there should be some additional distribution to those shares at some later stage.

With the company itself estimating that 10p is the cash value of the shares, I can make no argument against XLM’s 9.8p share price today. And I’m relieved that I stayed sceptical of the initial cash figure that I calculated last week (£18.9m) - taxes and shutting down costs are always bigger than I expect!

Niox (LON:NIOX)

Down 19.5% to 56.67p (£225m) - Response to Rule 2.7 announcement & Strategic Update - Graham - AMBER/GREEN

This is not a share we’ve covered regularly here in the past, perhaps because it’s in the life sciences sector. I see that NIOX is the company previously known as Circassia that traded under the ticker CIR.

The company makes medical devices for asthma diagnosis and management.

Today we learn that a PE buyout fund has decided to not proceed with an offer for it.

Further to the announcement made by NIOX Group plc ("NIOX") regarding a possible cash offer for NIOX by Keensight Capital ("Keensight"), Keensight confirms that, in light of the current macro-economic backdrop, it does not intend to make a firm offer for NIOX.

I’ve been looking through NIOX’s most recent annual report for clues as to the company’s exposure to the US-China trade conflict. Medical devices are not exempt from Trump’s tariffs at present.

My initial search isn’t coming up with much specific info, only broad statements. For example:

NIOX outsources a number of important functions to a range of suppliers. In particular, the Company’s products are manufactured and distributed by third parties.

Their recent full-year results announcement (1st April) contained no commentary on the potential impact of tariffs.

Response to today’s news: NIOX have discontinued their sale process and have also given the market a reassuring trading update:

As noted in the preliminary results announcement on 1 April 2025, the current year has started well. Sales growth in the first quarter for the Group as a whole was 18%. Net cash as at 31 March 2025 was £15.4m.

An updated outlook statement and confirmation that full-year expectations were unchanged would have been most welcome!

Graham’s view

I was an asthma sufferer myself which gives me an extra reason to support this company’s efforts to improve the diagnosis and management of this condition.

The recent results showed the company making a clean pre-tax profit of £7.8m, up from £4.1m in the prior year.

Pre-tax profit is set to grow strongly again in the current year, supported by revenue growth of 13%. Although with Q1 growth of 18%, maybe they can beat that forecast?

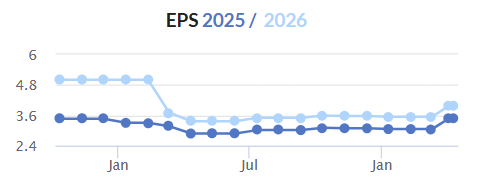

I note a recent uptick in EPS forecasts:

Although the share price is down today, that doesn’t seem to have anything to do with the specific performance of the company, although it likely does reflect macro risks that the company faces.

I’m leaning towards a positive view of this stock as, although expensive relative to earnings, the growth figures are promising and profits are becoming increasingly meaningful.

The company also seems to be shareholder-oriented, returning surplus cash to shareholders in a prompt manner. From the 2024 results statement:

The Board has decided to adopt a policy with regard to the return of cash to shareholders, given that for some time the Group has generated cash in excess of its investment needs. The first opportunity to utilise this policy is likely to be towards the end of the current financial year. Going forward, the Group will, on a rolling basis, return 80% of free cash flow to shareholders in the medium term, through ordinary dividend payments and additional cash returns.

In conclusion, I’m going to give this an AMBER. I would like to be more positive, but I need to temper my enthusiasm for a few reasons:

Even after today’s fall, the £225m market cap is a high multiple against forecast earnings over the next few years.

The potential PE buyers, having considered the risks in the current macro environment, have walked away.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.