In this week's Stockopedia Strategy Map article, Ed introduced the concept of Momentum. Momentum is the tendency for medium-term winners to keep doing well. A typical Momentum strategy looks at the share price performance from 12 months to one month ago. (In the very short term, share prices tend to mean revert rather than trend, so the last month is ignored.) A market-neutral strategy buys the top performers and shorts the worst performers, but a Momentum strategy can be implemented successfully on the long side only. Momentum is pervasive and has been shown to work across multiple time periods, geographies and asset classes.

It is generally accepted that Momentum generates excess returns because investors under-react to fundamental changes in company performance. This may be due to a psychological bias where investors dislike buying something they could have bought more cheaply earlier. I certainly suffer from this bias. However, the momentum effect may also be due to the under-reaction of company management to positive changes in their business performance.

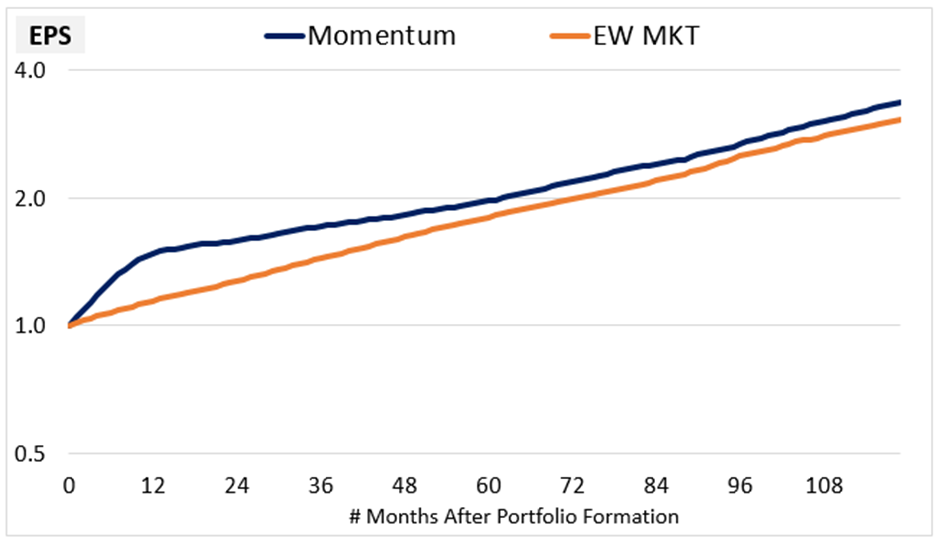

These effects are relatively short-lived. As this chart from a study called Factors from Scratch shows, high momentum stocks tend to exhibit higher than average EPS growth over the next year:

However, that the EPS growth ends up significantly below market averages after a year. Momentum strategies require regular rebalancing into the most recent winners.

In academic studies, Momentum has been shown to generate higher risk-adjusted returns than either Value or Quality, making it a key component of the Stockopedia StockRank. Unfortunately, there is a trade-off for this superior performance. The strategy undergoes periods of very rapid underperformance, so rapid they are known as Momentum Crashes.

Momentum Crashes

Momentum crashes tend to occur at the end of a bear market, when trends reverse rapidly, catching out those who rely on the recent price action to make investment decisions. As the 2022 study Isolating Momentum Crashes by Maik Dierkes and Jan Krupski, notes:

Since 1926, there have been several momentum crashes that feature short but persistent periods of highly negative returns. From June to August 1932 the momentum portfolio lost about 91%, followed by a second drawdown in April to July 1933. Another prominent crash took place in 2009 when Momentum lost more than 73% within a period of three months.

A 2016 paper called Momentum Crashes by Kent Daniel and Tobias J. Moskowitz…