I recently explained why I’m still buying UK shares despite the lure of 5% risk-free returns. In that piece I said that one segment of the market that looks particularly attractive to me at the moment is the FTSE 250.

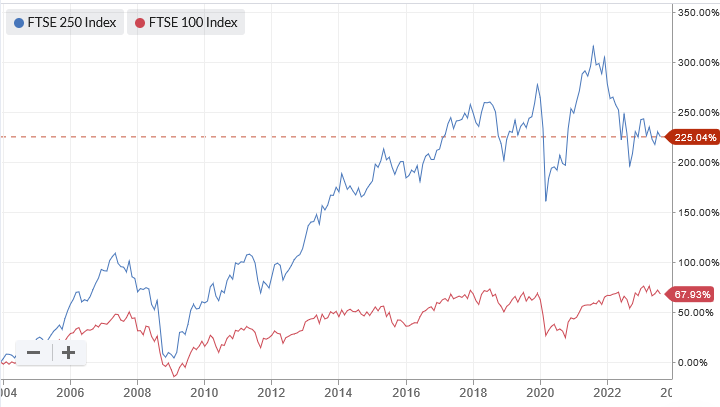

The UK’s mid-cap index is traditionally home to faster-growing companies than the FTSE 100. For much of the last 20 years it has also outperformed the FTSE 100 and been more expensive:

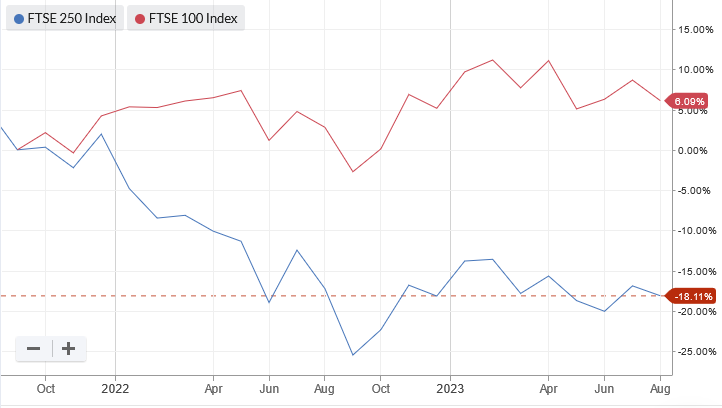

However, that picture has changed. The FTSE 259 has lagged behind the 100 over the last couple of years:

As a result, the FTSE 250’s valuation premium has disappeared.

According to Stockopedia data, the FTSE 250 now trades on just 12 times forecast earnings and offers a prospective dividend yield of 4%.

The equivalent figures for the FTSE 100 are 13 and 3.7%.

This matches up with my personal experience. A lot of the stocks that are catching my interest at the moment are FTSE 250 shares. Very few are in the FTSE 100.

I think it could be a good time to look for unloved but good quality companies in the FTSE 250. In the remainder of this piece I’m going to take a look at three stocks from this index with Contrarian ratings that I think look interesting today.

#1: CMC Markets (LON:CMCX)

This online financial trading firm has had a difficult year as trading activity (and profits) have come back to earth with a bump after the pandemic boom.

CMC warned on profits in March and the firm’s shares have fallen by 50% over the last year:

I reviewed CMC’s latest results in this SCVR in June, while Graham covered the firm’s Q1 update in July here. Both of us took a favourable view of the stock and suggested it could offer value at current levels.

While profits from the core leveraged trading business are down at the moment, this won’t last forever. CMC says that the level of client money and active client numbers “remain robust”, suggesting that clients are simply waiting for more favourable market conditions to return.

In the meantime, CMC is enjoying a sharp rise in interest income on…