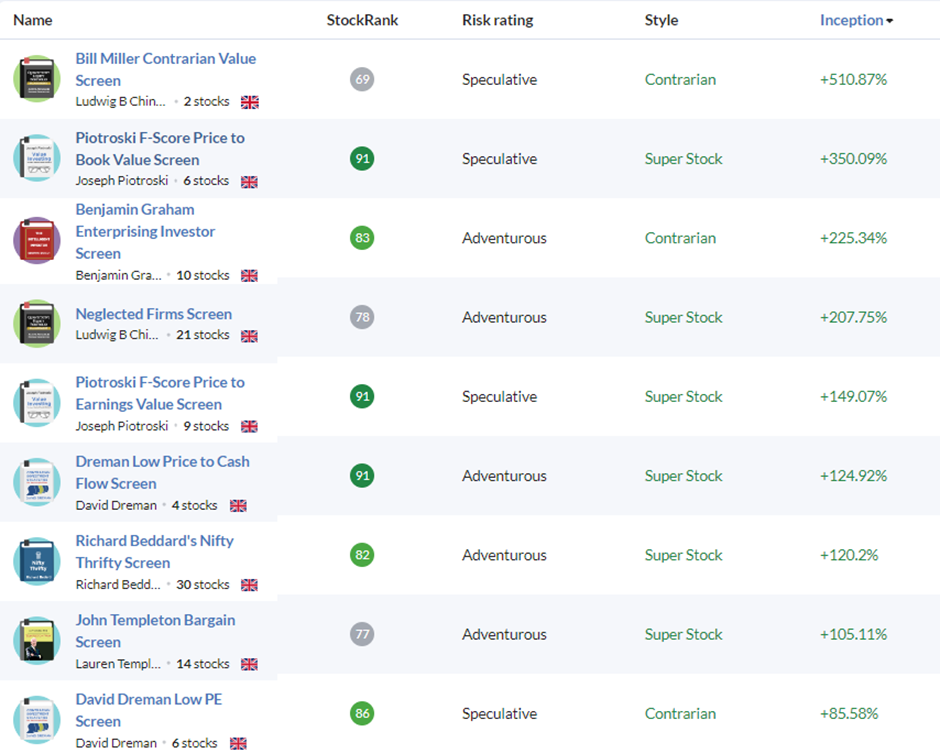

One of the challenges when screening for Value stocks is that many screens can generate very few results most of the time. For example, the current highest-performing Value-based Guru Screen in Stockopedia is the Bill Miller Contrarian Value. This screen has just two hits in the UK. Sadly, this makes the performance of this screen more dependent on chance than anything else.

Going down the list, the third best-performing Value Guru Screen is the Benjamin Graham Enterprising Investor screen based on the writings. This currently has ten results, making its 22% performance since inception more reliable. Graham said:

The determining trait of the enterprising investor is his willingness to devote time and care to the selection of securities that are both sound and more attractive than the average.

Much of Graham's investing focused on defensive strategies, using significant discounts to tangible assets, or even discounts to working capital to provide a margin of safety. However, this Enterprising Investor screen is less strict on valuation but adds requirements intended to generate higher returns over the long term. The screen results so far suggest it achieves this.

The Screen

Let's go through the criteria:

Cheap on both earnings and assets

Neither of these criteria is focused on finding companies that are the absolute cheapest on either earnings or assets, but together, they find companies that are fairly cheap on both metrics. This avoids companies that are highly profitable but lack tangible asset protection. This would include people businesses, such as recruiters or brokers, where the employees tend to end up generating the bulk of the returns to the business over the long term. Similarly, these criteria avoid businesses where there are a lot of tangible assets, but they are currently very unprofessional.

Conservatively financed

Value investing requires buying cheap stocks and waiting for them to become stock market darlings. For example, investors who recognised the potential of £ W7L's strategy in cosmetics at IPO in late 2016 had to wait six years before that strategy generated significant revenue growth and was reflected in the share price:

Companies that run out of money during the waiting period and dilute shareholders, or worse, go bust, never generate the…