Michael Sharp’s five years as the chief executive of Debenhams have not been an obvious success.

Mr Sharp’s spell at the helm included a string of profit warnings in 2013. His resignation came after reports that a number of major shareholders had been working with broker Cenkos to organise a boardroom shakeup.

A review of Debenhams’ financial performance suggests that City was right to campaign for change. Although Debenhams shares are worth 35% more than when Mr Sharp took charge in September 2011, profits are substantially lower. Net profit peaked at £125m in 2012 but was just £93.5m in 2015. That’s a 25% decline in just four years.

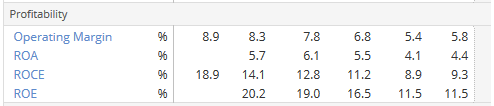

The big problem is that profit margins have fallen steadily. Debenhams’ operating margin was 8.9% in 2010. Today it’s just 5.8%:

This has been blamed on causes including excessive discounting and poor store sales versus online. The good news is that things may be about to change.

Debenhams already has a new chairman, Sir Ian Cheshire. Later this year, Debenhams will also have a new CEO. Until last year, Sir Ian was the chief executive of B&Q owner Kingfisher Group. He’s a highly-rated retail executive.

I believe that the combination of a new chairman and CEO could prove to be a catalyst for change. Indeed, I’d be surprised if something didn’t change. Debenhams’ fundamentals appear solid and suggest to me that this stock could be an attractive contrarian opportunity.

Classic value credentials?

What I like most about Debenhams is that it generates plenty of free cash flow. The shares currently trade on just 10.5 times trailing free cash flow. Last year’s surplus cash of 6.8p per share covered the 3.4p dividend twice, giving a very safe 4.6% trailing yield.

Debenhams scores well on other value metrics, too. A price/sales ratio of just 0.4 is undemanding, as is the trailing P/E of 9.5. I criticised the firm’s falling operating margins above, but Debenhams’ profitability isn’t quite as bad as its operating margin might suggest. The stock’s earnings yield last year (EBIT/EV) was 11.1%. That’s not too bad.

Despite this, there are a couple of risks I’d like to flag up. As the majority of Debenhams’ stores are leased, lease liabilities are considerable. According to the 2015 annual report…