Good morning! I'm kicking myself for having sold out of Kentz (LON:KENZ 472p) too early, as it has announced this morning a "highly conditional and unsolicited proposal" was received from Amec regarding a takeover at 565-580p.

Readers here will be well aware of what good value Kentz shares are, as it was flagged in my morning reports three times, on 3 May and 17 May at sub-400p, and again on 26 Jun. Readers who agreed with me, and bought the shares at that time, are already almost 20% up, and I suspect are likely to get another decent boost today on the rejection of the 565-580p takeover approach as it "undervalued the company" and has hence been rejected by the Board. So that both underpins the value at 472p per share, and could drive a higher takeover bid now the company is in play perhaps?

(Edit: I see Kentz shares are up 22% today, to 580p, which is great news for holders. Unfortunately, I forgot to include this one in Paul's Value Picks, which is a pity, as it was clearly a suitable candidate based on my Blog entries referred to above, but never mind - entries won't be altered or added retrospectively, as that would be wrong).

We're looking at a reasonable open, with the FTSE 100 futures indicating a rise of 19 points to 6,508.

I see the CEO of 21st Century Technology (LON:C21 6p) has fallen on his sword, which is probably a good thing given the profits warning and collapse in share price in the last fortnight. I picked up a few of these at just over 5.5p last week, as it seemed to have stopped falling, and if they drop again today then I might pick up some more. The Chairman says this morning that they are looking for a new CEO, and that:

We continue to pursue a number of exciting business leads and look forward to providing further updates in due course."

It strikes me that C21 is too small to be separately Listed, and has too lumpy sales, so this might be the ideal time for a larger competitor to put in a takeover approach for it.

Shares in 1pm (LON:OPM 42p) are now trading at a more sensible share price, following their share consolidation. The market price has gone from 0.3p per share to 42p per share, so I'll quickly check that it's correct.

The capital reorganisation is 146.67 old shares for 1 new share. So at 42p market price today, you just divide the "new money" price by 146.67 to get the "old money" share price, which in this case is 0.286p (old money). In this type of situation, I normally stick a post-it note on the edge of my screen, to remind me what the conversion factor is, during the period of a few days when your mind needs to adjust to the new share price.

Next I've been looking at (drum roll please!) interim results from Quindell Portfolio (LON:QPP 13p). As always, the headline figures look great - revenue increased 78% to £163.3m for the six months to 30 Jun 2013, although adjusted EPS only rose a comparatively small 17% to 1.1p, which I think is due to large number of shares having been issued, diluting the growing profits.

EBITDA increased by 44% to £47.7m, and profit before tax increased by 49% to £43.4m, so on the face of it very impressive numbers for the first half of the year.

The narrative says that:

"Average group trade debtor days at June 2013 reduced to circa 4.8 months (December 2012: 6.5 months)"

Cash collection was one of my main concerns with Quindell, as I have painful personal experience of losing my shirt a few years ago (about £250k loss) on Accident Exchange, which is in the same sector, and has made me very wary of the cash collection issue with this type of company. Accident Exchange reported fantastic growth, huge profits, but it all built up in debtors, which got longer & longer, and eventually had to be written off. So the profits were essentially fictitious in the long run. The shares collapsed, and they de-Listed.

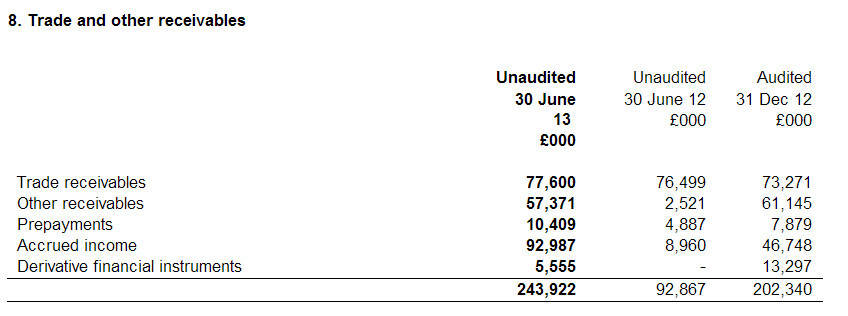

In Quindell's case, it all looks fine, as the above quote shows, trade debtor days have reduced to a reasonable 4.8 months. Or is it really fine? On checking the Balance Sheet, trade and other receivables are actually shown at £243.9m, which is considerably more than revenue for the six months of £163.3m. So how can debtor days be less than six months?

The answer can be found in note 8 to today's accounts, see below:

So trade debtors seems to be only a small part of total debtors. Accrued income is just debtors that have not yet been invoiced, and I have no idea what is in that £57.4m "other receivables" line. Prepayments and the derivative I can accept, so strip those out and you are still left with £228m in debtors, which is considerably more than six months turnover.

I don't know whether Quindell's services are VATable, but even if you add 20% VAT onto their entire H1 turnover, you still get to £196m, which is less than the £243.9m debtors figure. So my conclusion is that actually the jury is still out on whether Quindell can collect in its debtors, and that 4.8 months figure looks suspect to me - I'd like to know the workings of that number, as I don't think it includes everything it perhaps should? Anyway, the bottom line is that debtors are still growing and are still huge, so I'm not convinced.

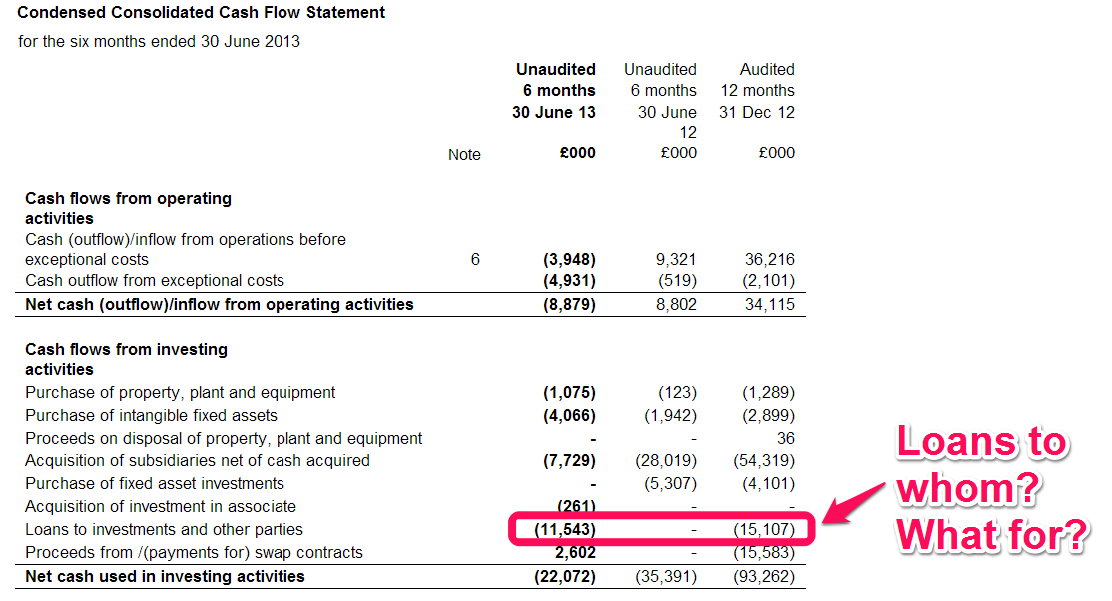

The cash position accordingly is not great. In fact, they still have net debt, of £14.1m, as once again all the growth has ended up in debtors. That should turn around at some point, when turnover growth slows, or goes backwards, but it's not generating cash at the moment.

Couple of other funnies jump out at me. On the cashflow statement there is another strange item, being £11.5m paid out, which is described as "loans to investments & other parties". What's that about then? I queried a similar item last year, of a £15.1m cash outflow, but nobody seems to know what that is either. These are quite material amounts, so who is Quindell loaning money to, and why? I'm not suggesting anything untoward, just querying it. See the extract from their cashflow statement below:

The company has issued a lot of shares in the past for acquisitions, and this looks set to continue, with long term liabilities including £24m in deferred consideration that has to be settled in shares. So expect ongoing selling from the various lock-ins expiring, which is certainly one of the drags on the share price.

My main concern though, is how sustainable Quindell's profits are? A contact in the insurance industry has told me that Quindell's profits are real, but that they are not sustainable. The company tries to pass itself off as being a technology business, whereas in reality it's an ambulance chasing business that is generating much of its profit from things like whiplash claims, which as we all know is a long-standing area of widespread falsification of claims by members of the public, who seem to regard it as fair game to claim for whiplash when they are in reality uninjured. At some point the insurers will stop this practice, and I'm surprised they have allowed it to go on this long.

So I just don't believe that Quindell has a sustainable business model at this level of profitability, but instead are almost certainly cashing in on recent regulatory changes, which have given them a purple patch whilst competitors scramble to catch up.

So I don't think it would be wise to base a valuation for the shares on a multiple of bumper profits which probably won't be sustained for that long.

This is probably why Quindell shares remain on such a low multiple of forecast earnings (PER of 5 for 2013, and 4 for 2014, based on Cenkos forecasts), as investors are collectively clearly not convinced the profits are sustainable.

Cenkos are convinced though, and I see their note this morning says they see the shares rising to 18p in the short term, and "potentially much higher (40p+)" in the longer term, so who knows? For me however, there are too many question marks over the business model, so it doesn't interest me as a potential investment. To clarify, I have never held a long or short position in Quindell, as I think it's just fundamentally too difficult to value accurately.

OK, that's it for today. See you from 8 a.m. tomorrow, and just a reminder that my 11 a.m. email goes out every day, to ensure you don't miss a morning report - sign up box is below, it just needs your email address, nothing else.

Regards, Paul.

(of the companies mentioned today, Paul has a long position in C21, and no short positions)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.