Building a Terry Smith portfolio with UK shares

Terry Smith’s annual letter to investors in his Fundsmith Equity Fund has become something of an event. He’s opinionated, informed, and usually has something spicy to say.

This year’s (2023's) letter came with an extra dose of anticipation, as we knew Smith would have to discuss why the Fundsmith Equity Fund fell in value and underperformed global equity markets last year. A rare event indeed. I started to wonder. If I tried to build a portfolio of UK shares Terry Smith might buy today, what might I end up with? Would they be companies I’d want to buy today?

I decided to build a stock screen to try and find out.

Reading the manual

One thing that Terry Smith and Warren Buffett have in common is that they don’t mind sharing details of their investment approach. Fundsmith provides an owner’s manual on its website that provides a very clear description of the kind of companies the fund buys, and the financial metrics on which Smith and his team focus.

To refresh my memory, I reread the owner’s manual and noted down the key criteria Fundsmith uses to assess stocks. I then checked the website for the fund’s current sector weightings and top holdings.

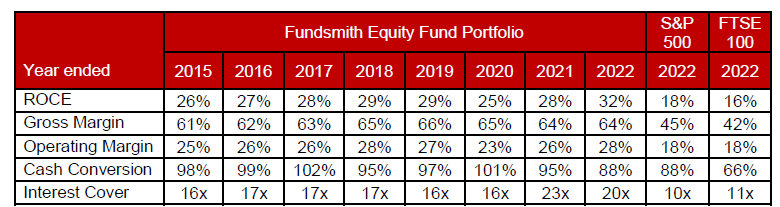

Finally, I looked at the table of portfolio financial metrics that’s always included in Fundsmith’s annual letter. This shows the weighted average financial characteristics of the fund’s portfolio, as if it were a single company.

Source: Fundsmith 2022 annual letter

Armed with this information, I built a screen which I think highlights stocks Smith might consider, if he restricted his investment universe to the UK instead of investing globally.

Terry Smith screening criteria

Fundsmith’s stated investment strategy is:

Buy good companies

Don’t overpay

Do nothing

In this section, I’ll explain how I’ve tried to translate this deceptively simple three-step process into a set of screening rules, using Smith’s letter and owner’s manual as a guide.

Sectors: The Fundsmith Equity Fund doesn’t have fixed sector allocations. Smith says he doesn’t pay much attention to sector weightings at any one time. However, the fund only invests in certain sectors of the market.

Broadly speaking, the fund aims to invest in companies that provide goods and services that are consumed in small quantities, at short and regular intervals. Consumer goods and online services are the obvious examples, but payment processors such as Visa (NYQ:V) are another example.

Heavily cyclical sectors are excluded, as are businesses selling capital goods that tend to generate lumpy revenues. Property and most financials are also ruled out, as these businesses tend to require leverage in order to generate satisfactory returns.

Smith doesn’t mind leverage, but he doesn’t like companies that can’t function without it. Banks and property are typical examples of this, but interestingly he also includes retailers’ large store lease liabilities in this category as well.

This approach is convenient for UK investors, because operating leases are included in statutory net debt under IFRS 16 rules. That means we can easily use this figure in our screening without needing to consider adjustments.

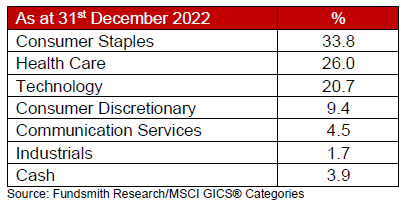

Here’s how the Fundsmith Equity Fund was positioned at the end of 2022:

Source: Fundsmith 2022 annual letter

I’ve translated this to the following UK market sectors, using Stockopedia’s classifications:

Consumer defensive

Consumer cyclicals

Technology

Telecoms

Healthcare

Industrials (I’ve included this as some stocks from this sector could be relevant)

Business characteristics: Smith looks for businesses that are able to generate sustainable, above-average returns on capital employed. This is more unusual than it might seem.

In most cases, above-average returns attract additional capital into a sector, thereby driving down future returns to more average levels. This is known as mean reversion. It’s a common phenomenon in the financial markets – it often applies to valuations, as well.

Smith’s approach to this problem is to focus on businesses that have intangible assets providing some kind of lasting competitive advantage. These might include:

Brands and intellectual property

Hard-to-replicate distribution networks

Large installed base of users

Dominant market share

Valuable client relationships

Profitability: Fundsmith’s primary measure of profitability is return on capital employed. I share Terry Smith’s view that this is the only measure that reliably captures the value created by a company for its shareholders (excluding financials, where return on equity is often more appropriate).

Other complementary profitability metrics that are used by Fundsmith are gross margin and operating margin. I’ve included operating margin in my screen, as I find it’s a more consistent metric for screening across different sectors.

Valuation & growth: Even a great business can become a below-average investment if we pay too much for it. This is why “don’t overpay” is such an important part of Fundsmith’s strategy.

The main valuation measure used by the fund is free cash flow yield. In the owner’s manual, Smith says his aim is to invest in companies with free cash flow yields that are “high relative to long-term interest rates and when compared with […] other investment candidates” such as bonds.

The idea is that the fund will buy equities with free cash flow yields that are equal to or greater than bond yields. The equities will then grow and compound in value over time, outperforming bonds, which can’t compound.

Growth is obviously a key element of this, so I’ve also included free cash flow growth – the measure used by the fund – in my screen.

Finally, I’ve specified a minimum market cap of £500m. Fundsmith Equity Fund is a big cap fund, so I don’t want to include small caps in my results.

Terry Smith Fundsmith screen

When creating a screen, there’s always a temptation to over optimise. I’ve tried to avoid this. I want the screen results to provide a plausible menu from which I can choose, not a prescriptive list of stocks to buy.

Here are the rules I’ve used, based on the criteria discussed above:

Economic sector includes consumer cyclical, consumer defensives, technology, telecoms, healthcare and industrials

Long-term average ROCE greater than 14%

Operating profit margin (TTM) greater than 15%

Net debt less than five times TTM net profit

Interest cover (TTM) greater than 10x

Price to free cash flow (TTM) less than 30 (equivalent to 3.3% FCF yield)

Free cash flow 5y growth rate greater than 0%

Market capitalisation greater than £500m